巴菲特致合伙人的信(1963年半年度)

①业绩②基金公司

1963 年 7 月 10 日

上半年业绩

1963 年上半年,道指从 652.10 上涨到 706.88,加上 10.66 美元的股息,道指的整体收益率是 10.0%。

我们又要老生常谈了:

(1)三年以下的短期业绩毫无意义,我们有一部分投资是控股类, 短期业绩对我们更没意义。

(2)与道指和公募基金相比,在市场下跌时,我们能跑在前面, 在市场泡沫中,我们可能望尘莫及。

尽管如此,不算登普斯特的估值变化,我们上半年的业绩是上涨 14%,其实登普斯特的估值有变化,这个好消息我留到后面再说。14%是按照总净资产计算出来的(包括登普斯特的资产),其中扣除了经营费用,未扣除有限合伙人利息和普通合伙人分成。短期的分成计算只是纸面上的,如果我们年末确实上涨了 14%,则先把 6%按照各自的本金占比分配给合伙人,再把剩下的 8%中的四分之三,即 6%,分配给合伙人,有限合伙人合计获得 12%的收益率。

虽说我们上半年的相对业绩喜人,第二段中的提醒仍然完全有效。我们今年上半年的业绩不如 1962 年上半年。今年上半年,我们上涨 14%,道指上涨 10%;1962 年上半年,我们下跌 7.5%,道指下跌 21.7%。这个思维方式,我们在上一封信中重点讲过了,大家必须彻底明白。

上半年,我们“低估类”的净投资金额(低估类中做多仓位减去做空仓位)约为 5,275,000 美元。低估类净投资带来的整体收益是 1,100,000 美元,低估类收益率约为 21%(关于我们的三种投资类别,请参考去年的年度信)。这再次证明我们在各个类别中的配置会影响短期业绩。1962 年,低估类是亏损的,因为套利类和控制类表现出色,我们才能取得不俗的收益率。

今年,套利类的收益不如道指,拖累了我们的业绩,这种情况在市场上涨时很正常。在市场上涨时,100%持有低估类,在市场下跌时,100%持有套利类,那当然好了,但是我不猜测市场走势来安排仓位。我们觉得,从长期来看,我们的三类投资都很赚钱,虽然在不一样的市场行情中,它们的短期价格表现迥然不同。我们认为,从长期来看,揣测市场波动赚不着钱,我们不猜涨跌,不直接猜,也不间接猜。猜测哪一类投资短期内表现最好,就属于间接猜。

基金公司

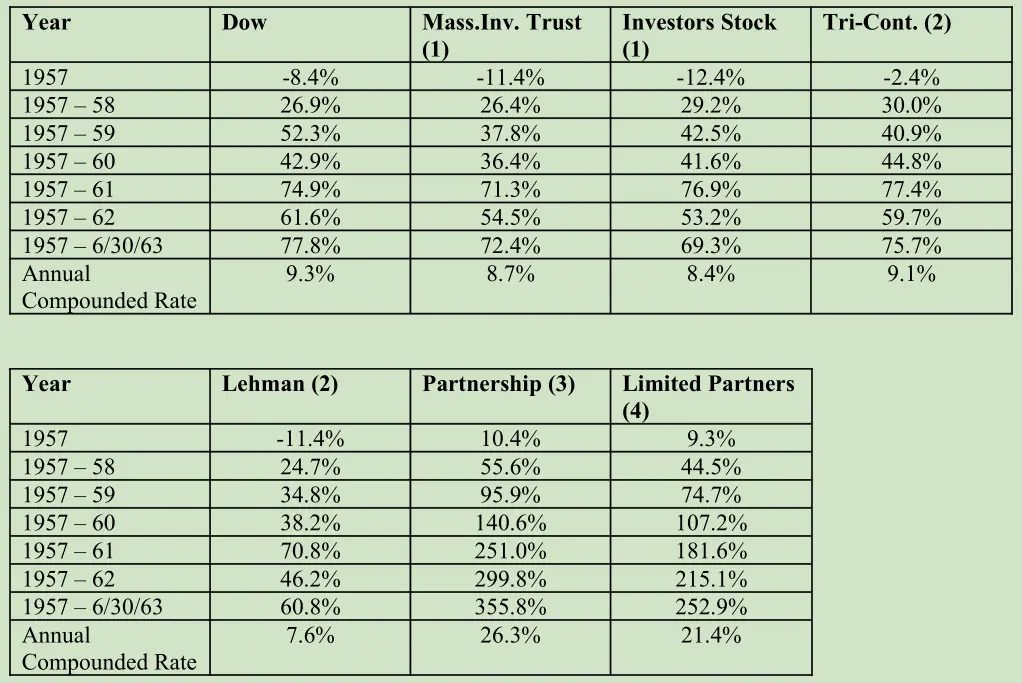

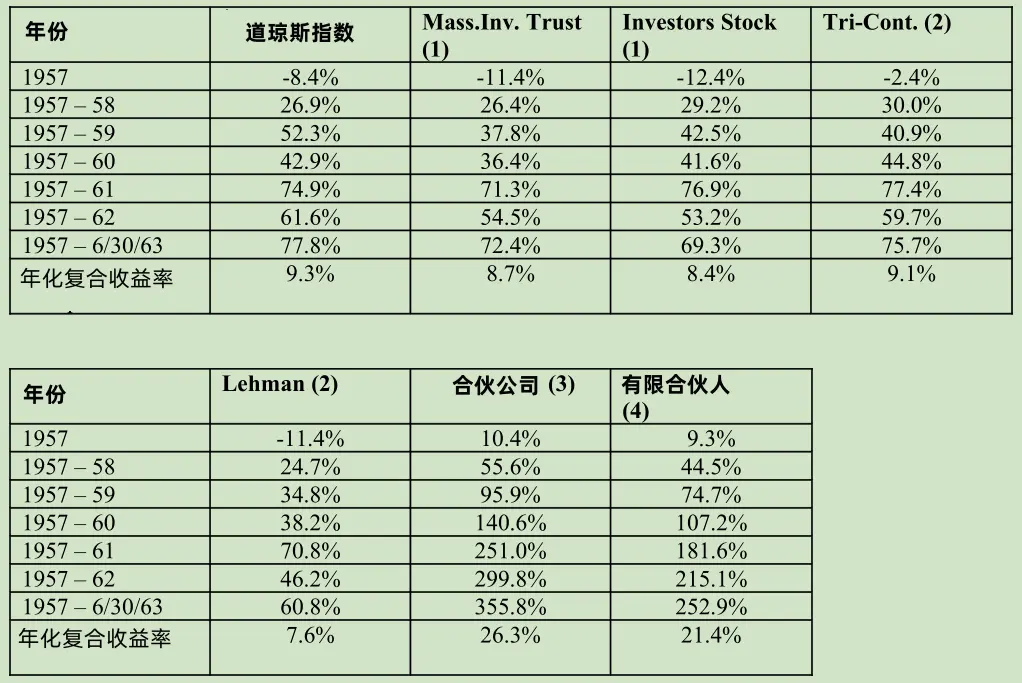

与往常一样,下表是道指、我们的合伙基金(包括先前的合伙人账户)、两家最大的开放式基金以及两家最大的分散投资股票的封闭式投资公司的复合收益率对比情况。

备注:

(1)计算包括资产价值变化以及当年持有人获得的分红。

(2)来源:1963 Moody's Bank&Finance Manual for 1957-62。1963 年上半年数据为估算值。

(3)1957-61 年的数据是之前全年管理的所有有限合伙人账户的综合业绩,其中扣除了经营费用,未计算有限合伙人 利息和普通合伙人分成。

(4)1957-61 年的数据以前一列合伙基金收益率为基础,按照当前合伙协议计算,扣除了普通合伙人分成。

大基金费用高昂、地位尊崇,道指是无人管理的一揽子蓝筹股,但是我们从业绩对比中可以看出来,大基金始终跟不上指数。投资顾问、信托部门和大基金的方法、逻辑类似,业绩也差不多。我不是要批评这些机构。这些投资途径为数千万投资者提供了大量服务,包括高度分散、方便省心、避开劣质股等,但是它们的服务不包括(绝大部分基金也没承诺)以高于大盘的收益率让资金复利增长。

归根到底,我们合伙投资是为了什么?就是为了与一般投资途径相比,我们能以更低的长期本金损失风险,实现更高的复利。我们保证不了一定能实现这个目标。我们能肯定的、能保证的是,在相当长的一段时间内,只要不是投机热潮无休无止,如果我们还实现不了这个目标,我们就清盘。

〔译文来源于梁孝永康所编全集〕