巴菲特致股东的信(1976年)

③保险投资业务④银行业⑤蓝筹印花公司⑥杂项

保险投资情况

1976年随着可投资资产在更高的保费收入和更好的盈利之下的显著增长,保险投资的税前投资收入从8,918,000美元上升到10,820,000美元。

在最近的报告中,我们提到了债券账户上的浮亏,但我们认为这些市场波动的影响是次要的,因为我们的流动性和财务实力使我们不太可能在不恰当的时机卖出这些债券。在1976年,债券市场大幅上扬,这使得我们的银行和保险公司拥有的债券组合的年末未实现收益有微幅上升。这也是次要的,因为我们打算把大部分债券持有到期。较高债券价格的必然结果是再投资收益的下降。总的来说,我们更喜欢我们的债券市值小于其账面价值。这样再投资时就能获得更有吸引力的利率。

去年,我们提到我们期望1976年会实现资本收益。事实上,我们在1976年获得了主要来自股票投资的996.2万美元的税前资本收益。现在看来,1977年同样是实现净资本收益的一年。目前我们的股票组合中有一大笔未实现资本收益,而几年前我们的股票组合中有大笔的未实现亏损。我们依然认为每年都在发生的市场波动相对而言是不重要的;我们股票组合中的未实现资本收益,年终高达4570万美元,在我们3月21日写这封信时已经下降了500万美元。

然而,我们认为所投资公司业务的进展是重要的。1976年,我们对所投资公司的优秀业绩表示满意。如果公司未来几年业绩继续如此出色的话,我们肯定能从股票投资中取得丰厚的回报,而每年的股市波动是无关紧要的。

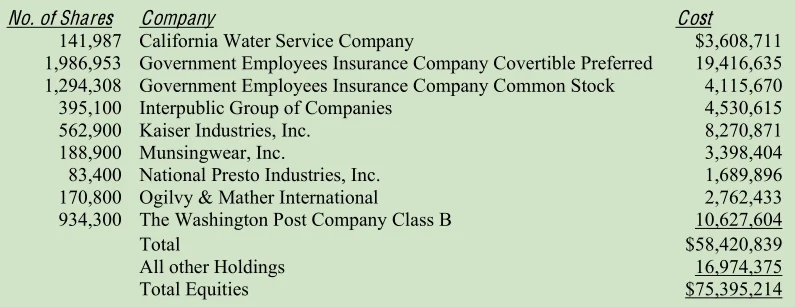

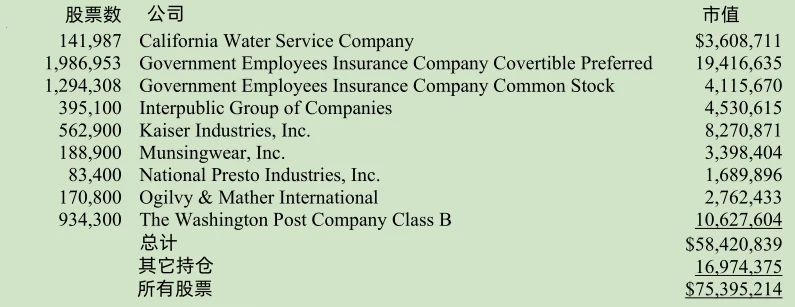

我们在1976年12月31日持有的超过300万美元的投资如下:

你会发现,我们的主要持股相对较少。我们基于公司的长期表现进行投资,并会仔细考虑如果整个收购公司所要考虑的因素:

(1)对公司有利的长期经济因素;

(2)有能力且忠诚的管理层;

(3)以整个收购企业的标准来度量,价格有吸引力;

(4)是我们所熟悉的行业,我们能判断其长期的经济特征。

寻找到符合我们标准的公司很困难,这也是我们喜欢集中持股的原因之一。我们无法找到一百只满足我们投资标准的股票。然而,我们觉得集中持有少量我们已确认有吸引力的股票是非常舒适的。

我们打算长期持股,但有时我们也做短线投资,如对凯撒工业的投资。该公司预计1977年母公司将进行现金红利和股票红利的分配。在该公司管理层宣布了红利分配方案后,我们在1976年买入了这家公司的股票。

银行业务

Eugene Abegg我们附属银行伊利诺伊国民银行和伊利诺伊州的罗克福德信托投资公司的总裁继续引领银行界——正如他在1931年银行刚成立时所做的一样。

最近,克利夫兰国民城市公司,一家拥有真正出色管理的银行在一则广告中写道“1976年我们平均资产收益率为1.34%,我们相信这是在所有主要银行公司中的最好水平。”在真正的大银行中这是最好的盈利业绩,但伊利诺伊国民银行的盈利比国民城市公司的盈利水平要高出接近50%,平均资产收益率大约为2%。

这一优秀的盈利记录在以下措施的作用下再次被实现了:

(1)对所有消费储蓄支付了最大利率(定期存款超过了总存款的三分之二);

(2)保持了良好的流动性(出售的联邦基金加上目前买入的六个月以下美国政府债券大约等于活期存款总额);

(3)避免高利率的低劣贷款(1976年贷款坏账约为12000美元,或着说0.02%的坏账率。这与1976年的银行界的现行坏账率相比非常小)。

成本控制是银行成功的重要因素。该银行的雇员数量仍然保持在1969年购买它时的水平,尽管消费定期存款从3000万上升到9000万并在信托、旅行支票和数据处理等其他业务上有显著的扩张。

蓝筹印花公司

1976年我们增加了在蓝筹印花公司的权益,年底前我们已持有该公司33%的流通股。蓝筹印花的股权对我们日益重要。蓝筹印花的财务报告摘要在我们所附的财务报表的脚注里。另外,伯克希尔哈撒韦公司的股东可以从蓝筹印花公司的董事长秘书Robert H.那里得到现在和后续的年报。他的地址是加利福尼亚州洛杉矶东南大道5801号蓝筹印花公司,邮编90040。

杂项

伯克希尔哈撒韦公司的子公司K&W第一年已表现出不错的业绩,销售额和利润较之1975年均有适度增长。

我们只有不到四年的时间按规定的在1980年12月31日之前把我们的银行部门剥离出去。我们打算以一种对我们银行部门损害最小的方式完成这种剥离并为股东赢得最大利益。最大的可能是我们以分拆上市的办法在1980年把我们的银行部门剥离出去。

我们也希望在合适的时候对多元化零售公司进行合并。无论对蓝筹印花公司的整合还是持股的增加都使这次并购有利可图。然而,希望与并购相关的各项任务都在1977年推行是不可能的。

沃伦.巴菲特,董事会主席

1977年3月21日

〔译文来源于梁孝永康所编《巴菲特致合伙人+致股东的信全集》〕